Harvesting the

Volatility Risk Premium.

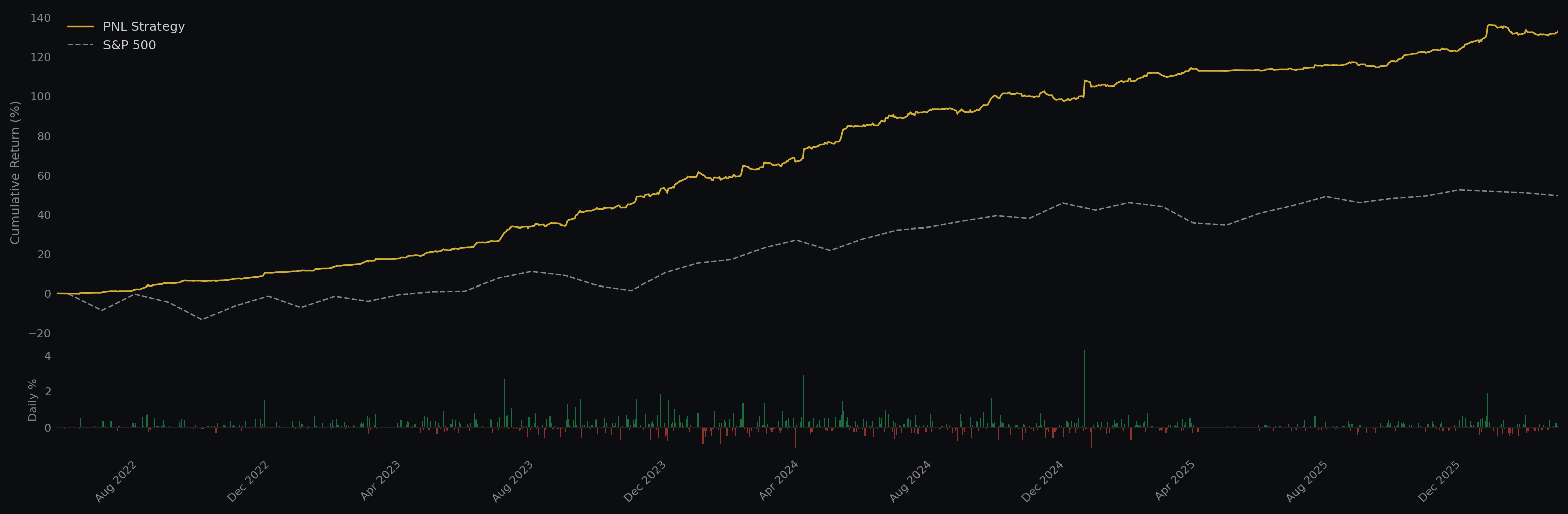

A systematic operation engineered around the structural gap in same-day SPX options, where implied volatility persistently exceeds realized. Designed first to survive the worst week, not to chase the best one.

Defined risk · Mechanical sizing · Automated execution · Same-day exit

The Edge

Options Markets Persistently Misprice Volatility.

Decades of research show that implied volatility tends to exceed realized volatility. Institutions pay to hedge, retail buyers overpay for protection, and market makers demand compensation for inventory risk. The "volatility risk premium" is not a market inefficiency. It is a structural feature, harvested under strict risk constraints, not pursued for its own sake.

Risk Discipline

- Defined-risk structures only

- Per-trade loss caps set in advance

- Same-day expiration removes overnight exposure

- Mechanical position sizing, no discretion

Systematic Process

- Multiple uncorrelated sub-strategies

- Live data driven execution

- Rules-based risk management

- No discretionary overrides

Investor-Friendly Structure

- Managed account at your broker

- You maintain full custody

- Complete position transparency

- Pooled vehicle available for select investors

Process

Engineered Around One Constraint.

Defined

Risk Per Trade

No naked positions

Daily

Re-Marked

Re-priced each morning

Mechanical

Position Sizing

Rules, not feel

Automated

Execution

Removes emotion

Detailed track record, attribution, and risk documentation are released to qualified investors on request, under NDA.

Process

How It Works.

Open Your Broker Account

Fund an account at a supported broker (TastyTrade, Interactive Brokers, TradeStation, Tradier, or Schwab). You maintain full custody and control. The operation never holds or moves your funds.

Grant Trading Authority

Sign a Limited Power of Attorney for trade execution only. You can revoke access at any time. No withdrawal authority, no access to personal information.

Automated Execution, Full Transparency

The systematic operation runs daily under pre-set rules. You see every position in real time through your broker. Weekly reports cover positioning and risk usage.

From the Founder

A Practitioner's Guide to Systematic 0DTE.

The book sets out the methodology behind the operation: why the volatility risk premium exists, how iron condors are constructed, how positions are sized, and how risk is contained. Written for readers who care about the reasoning, not the marketing.

About

Mark Uretsky

Founder, PNL Capital Partners

From the founder of a systematic trading operation focused on options market microstructure. The work is grounded in the academic literature on the volatility risk premium and refined through years of live execution.

The operation runs on infrastructure built specifically for same-day SPX execution: live data, mechanical entry and exit rules, and risk controls that the system cannot override.

He is the author of "0DTE: Extracting the Volatility Risk Premium Through Same-Day Options", which documents the methodology in full. The book covers the reasoning behind the edge and the discipline required to keep it.

Ready to Learn More?

A short call to walk through the operation, review the track record under NDA, and assess fit. Conversation, not a pitch.